This means you can rotate your companys inventory by selling its oldest units first and yet flow the costs by using LIFO or weighted average. Uses the FIFO inventory cost flow assumption.

Solved Proponents Of The Lifo Inventory Cost Flow Assumption Chegg Com

When a firm uses the LIFO inventory cost flow assumption.

. Net income will be greater than if FIFO were used. One of the principal reasons for selecting the LIFO cost flow assumption instead of the FIFO cost flow assumption in an inflationary economic environment is that. LIFO is used during inflation to defer income tax payments.

Cost of goods sold will be the same as if FIFO were used. LIFO results in significantly understated inventory values assets if it has been used for. You must also realize that the cost flow assumption is independent of the physical flow of the products.

Cost of goods sold will be greater than if FIFO were used. Uses the FIFO inventory cost flow assumption. However because of tax law requirements if a company uses this assumption for tax purposes it must also use it for its financial statements.

Thus the gross profit would be 11 and the ending inventory would be 27 13 14. Since this is the highest-cost item in the example profits would be lowest under LIFO. In a year of rising costs and prices the firm reported net income of 255987 and average assets of 1412450.

The inventory cost flow assumption describes the flow of product cost. A higher selling price can be established. LIFO conformity rule It does not coincide with the actual movement of goods.

If Mannisto had used the LIFO cost flow assumption in the same year its cost of goods sold would have been 300000 more than under FIFO and its average assets would have been 300000 less than. Uses the FIFO inventory cost flow assumption. Uses the FIFO Inventory cost flow assumption.

Cost of goods sold will be greater than if FIFO were used. Net income will be higher. C cost of goods sold will be the same as if FIFO were used.

Last in first out LIFO is a method used to account for how inventory has been sold that records the most recently produced items. Balance sheet inventory values will be higher. If Monnisto had used the LIFO cost flow assumption in the same year its cost of goods sold would have been 44210 more than under FIFO and its average assets would have been 34150.

Thus the gross profit would be. In a year of rising costs and prices the firm reported net income of 219138 and average assets of 1552940. When a firm uses the LIFO inventory cost flow assumption.

In the preceding example the May 24 unit would be assumed to have been sold. Net income will be greater than if FIFO were used. When a firm uses the LIFO inventory cost flow assumption better matching of revenue and expense is achieved than under FIFO The allowance for uncollectible accounts is an.

A cost of goods sold will be greater than if FIFO were used. Accounting questions and answers. The weighted-average cost would mean that both the inventory and the cost of goods sold would be valued at 105 per unit.

Income taxes will be lower. Better matching of revenue and expense is achieved than under FIFO Accounts receivable are reported at. Better matching of revenue and expense is achieved than under FIFO.

There is better matching of revenue and expense is achieved than under FIFO. When a firm uses the LIFO inventory cost flow assumption. B net income will be greater than if FIFO were used.

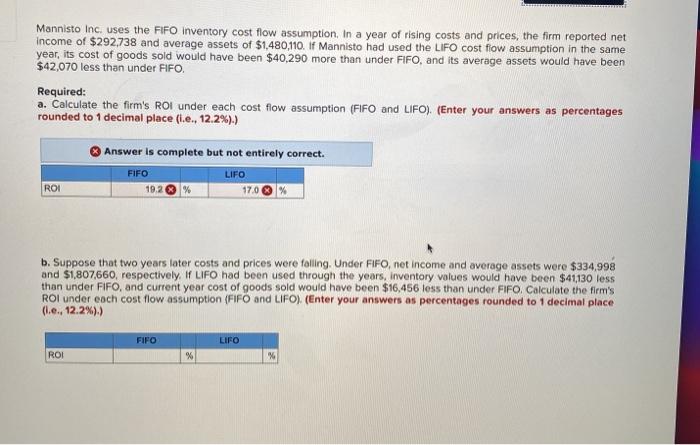

From the asset inventory account and to the expense cost of goods sold account. In a year of rising costs and prices the firm reported net income o 212357 and average assets of 1554120. Total current assets are not affected.

A cost of goods sold will be greater than if FIFO were used. D better matching of revenue and expense is achieved than under FIFO. Thus the cost of goods sold would be 90.

If Mannisto had used the LIFO cost flow assumption in the same year its cost of goods sold would have been 47840 more than under FIFO and its average assets would have been 41360. Under LIFO the goods in. Under the last in first out method you assume that the last item purchased is also the first one sold.

Cost of goods sold will be the same as if FIFO were used. Disadvantages of LIFO. When a firm uses the LIFO inventory cost flow assumption.

Over the life of the firm the total cost of goods sold for financial reporting and tax purposes must be equal to the total price paid for inventory. Under the last-in first-out LIFO inventory cost flow method the last units purchased are assumed to be sold and the ending inventory is made up of the first purchases. One of the principal reasons for selecting the LIFO cost flow assumption instead of the FIFO cost flow assumption in an inflationary economic environment is that.

Better matching of revenue and expense is achieved than under FIFO. Better matching of revenue and expense is achieved than under FIFO. If Mannisto had used the LIFO cost flow assumption in the same year its cost of goods sold would have been 35110 more than under FIFO and its average assets would have been 31140.

B net income will be greater than if FIFO were used. LIFO cost flow assumption. When a firm uses the LIFO inventory cost flow assumption.

This cost flow assumption was developed for tax purposes. In a year of rising costs and prices the firm reported net income of 1500000 and average assets of 10000000. Inventory cost presented on the Balance Sheet is not close to current value.

When a firm uses the LIFO inventory cost flow assumption. Cost flow assumptions are timing issues. When a firm uses the LIFO inventory cost flow assumption.

Solved Mannisto Inc Uses The Fifo Inventory Cost Flow Chegg Com

Solved Mannisto Inc Uses The Fifo Inventory Cost Flow Chegg Com

Solved Mannisto Inc Uses The Fifo Inventory Cost Flow Chegg Com

0 Comments